How a Scholar's Challenge Made CoinStudy's Methodology More Honest

CoinStudy does not claim to be infallible.

We claim to be honest. We claim to be transparent. And we claim that when a valid challenge reveals a genuine gap in our methodology, we will address it openly rather than quietly hoping nobody notices.

This blog is about exactly that kind of moment.

Over the past two weeks a reader named Ali raised a precise and legitimate fiqh challenge about how CoinStudy labels certain red-line violations. His challenge led to a meaningful improvement in our methodology that affects how we evaluate every exchange token, every DeFi protocol, and every blockchain ecosystem on our platform.

Muslim investors deserve to understand what changed, why it changed, and what it means for the analyses they rely on.

The Challenge That Started This

Ali's question was specific and fair.

If BNB the token itself does not involve a loan, does not pay guaranteed interest, and does not inherently require participation in futures or leverage, why are "Riba Exposure" and "Guaranteed Interest" treated as direct red-line violations rather than secondary concerns about ecosystem exposure?

He raised a similar point about Uniswap LP, arguing that LP is not a classical lending arrangement, returns are not guaranteed, and general speculation alone does not constitute Maysir in classical fiqh.

Both challenges pointed to the same underlying methodological question. CoinStudy's red-line labels were sometimes describing token-level concerns and sometimes describing ecosystem-level concerns without clearly distinguishing between the two.

That lack of precision was a genuine gap. Ali identified it correctly.

Why the Labels Mattered

In Islamic finance, labeling matters because it affects how Muslim investors understand the nature of a concern.

When a label says "Riba Exposure" on a coin analysis, a reader naturally understands that the token itself involves interest-based financial mechanisms. That is an accurate description for something like USDT, where the token's reserve backing directly generates interest income that funds the entire stability mechanism.

But for BNB, the situation is different. BNB the token does not charge interest. BNB does not create a lending relationship. BNB does not pay guaranteed returns to holders.

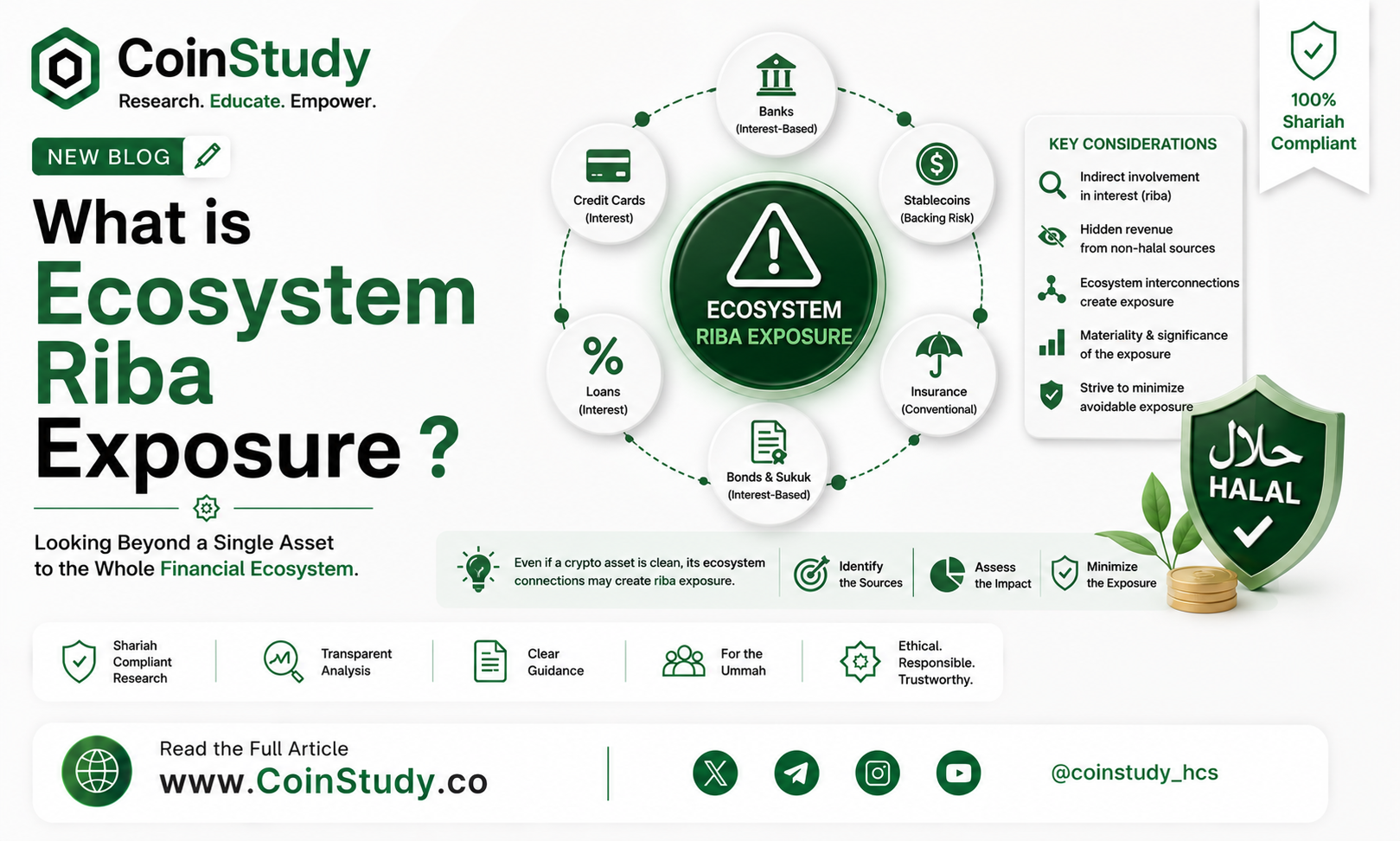

The compliance concern for BNB is that the Binance ecosystem, whose growth directly drives BNB's value, generates significant revenue from interest-bearing earn products, lending programs with advertised APY rates, and perpetual futures markets with leverage financing fees. BNB benefits economically when these prohibited products grow. That connection is structural, documented, and inseparable from BNB's economic value proposition.

This is a real and serious compliance concern. But it is ecosystem-level Riba exposure, not direct token-level Riba exposure. Using the same label for both situations without distinction created confusion about the nature of the concern.

The Distinction That Clarifies Everything

Understanding the difference between direct Riba exposure and ecosystem Riba exposure is essential for Muslim investors evaluating any token.

Direct Riba Exposure exists when the token itself is built around interest-based financial mechanisms. USDT holds Treasury bills that generate interest income funding the peg. GHO is minted through interest-bearing debt positions on Aave. Ethena's USDe generates yield through perpetual futures funding rate arbitrage. In these cases the prohibited mechanism is at the core of what the token is and does. You cannot hold the token without being directly connected to the interest-based mechanism.

Ecosystem Riba Exposure exists when the token itself is not an interest-bearing instrument but derives its value from an ecosystem that generates revenue through prohibited financial activities. BNB is not a lending product but its value grows when Binance's lending products grow. Exchange tokens across our analysis series share this characteristic. Their compliance concern is the inseparable economic connection between the token's value and the prohibited activities of the ecosystem it represents.

Both types of exposure are genuine compliance concerns under CoinStudy's HCS methodology. But they are different in nature and they deserve different and more precise labels.

What CoinStudy Changed

Following Ali's challenge and our internal review, CoinStudy has updated its red-line screening framework with one specific and meaningful change.

The red-line factor previously labeled "Riba Exposure" is now labeled "Ecosystem Riba Exposure" across all coin analyses on the platform.

This single label change makes the methodology more precise in two important ways.

First, it clarifies that the concern covers both direct token-level Riba and indirect ecosystem-level Riba exposure under a single comprehensive screening criterion. A token fails this red line whether its Riba concern is direct, like USDT's Treasury bill reserves, or ecosystem-level, like BNB's connection to Binance's lending products.

Second, it more accurately describes what CoinStudy actually evaluates. Our methodology has always evaluated tokens within their full ecosystem context rather than in isolation. The updated label reflects this approach transparently rather than implying a narrower token-level evaluation.

Why Ecosystem-Level Evaluation Matters

Some investors argue that a token should be evaluated purely on its own technical design rather than on what the broader ecosystem does. This is a legitimate methodological position and some Islamic finance platforms adopt it.

CoinStudy's position is different and the reasoning is principled.

A token cannot be economically separated from the ecosystem whose growth drives its value. When you hold BNB, your investment benefits when Binance grows. When Binance grows through its lending products and earn programs, your BNB appreciates because of that Riba-generating activity. The economic connection is not incidental. It is structural and documented.

Islamic finance has a well-established principle that benefits derived from prohibited activity carry the compliance concern of that activity. A person who profits from a business activity does not escape compliance responsibility simply because they hold a governance token rather than running the business directly.

Applying this principle consistently means evaluating tokens within the context of the ecosystems that drive their economic value. That is what CoinStudy has always done. The updated label now describes this approach more precisely.

What This Means for Existing Analyses

The label change affects the presentation of many analyses on CoinStudy. It does not change any verdicts.

Exchange tokens including BNB, HTX, KCS, OKB, BGB, LEO, CRO, and GateToken remain classified as Haram. The substantive reason for those classifications remains the same. The label describing that reason is now more precise.

Tokens that previously failed "Riba Exposure" due to direct token-level interest mechanisms, including all thirteen stablecoins in our analysis series, retain the same classification for the same reasons. Their Riba exposure is both direct and ecosystem-level simultaneously.

Tokens that passed the previous Riba Exposure check retain their passing status under the updated Ecosystem Riba Exposure label.

No scores changed. No verdicts changed. One label became more precise.

The Broader Principle This Illustrates

CoinStudy's methodology is not a closed document published once and never revised. It is a living framework that improves through genuine scholarly engagement.

Ali's challenges led to two specific improvements in a two-week period. The UNI analysis was updated to reflect the December 2025 UNIfication structural change and to more clearly distinguish between holding UNI as a governance token and actively providing liquidity. The Riba Exposure label was refined to more precisely describe ecosystem-level evaluation.

Both improvements make CoinStudy's methodology more accurate, more defensible, and more useful for Muslim investors trying to make genuinely informed decisions.

This is how Islamic finance scholarship is supposed to work. Questions are raised. Evidence is examined. Methodology improves. Conclusions are updated when the evidence warrants it and maintained when it does not.

CoinStudy is not the final word on any of these questions. We are one voice in a broader scholarly conversation that the Muslim investor community deserves to have access to. Our commitment is to make that voice as honest, as precise, and as intellectually rigorous as we can.

When a scholar identifies a genuine gap, we close it. When a verdict is challenged without new evidence, we explain our reasoning. When we are wrong, we say so.

That is the standard CoinStudy holds itself to. And we are grateful to every member of our community who holds us to it.

Final Note to Ali

Your challenges made CoinStudy's methodology better. Whether that was your intention or not, the outcome has been genuinely constructive. Two improvements to a platform that serves Muslim investors across eight countries came directly from your engagement.

That is what principled scholarly dialogue is supposed to produce.

JazakAllah Khair.

Read detail analysis of following coins here:

Is USDT Halal?

Is BNB Halal?

Is HTX Halal?

Disclaimer: This article is provided for educational and research purposes only. CoinStudy does not provide personal financial or religious rulings. Investors should consult qualified Islamic scholars for individual guidance.